The markets are struggling, what should you do?

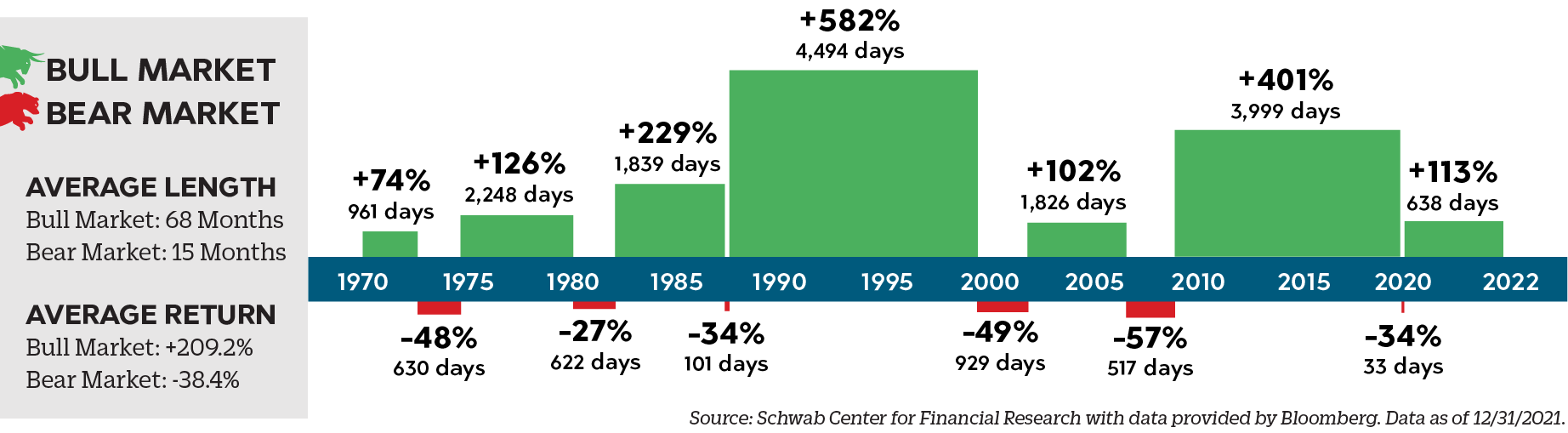

If you’ve been paying attention to the markets, you already know that it has been a bumpy ride lately. So what should you do? Buy? Sell? Panic? Bury your money? While the options are endless, there’s one, consistent strategy that is typically recommended in these types of situations: stick to your long-term strategy, stay invested, and wait it out.

Early Career Employees – 15 or more years until retirement

Everyone dreads a down market, but if there’s any group of people who should look at this event and see potential dollar signs, it’s those who have decades until retirement. Market downturns can provide long-term investors with opportunities to buy investments while prices are low and set themselves up for a bigger payday down the road. Remember, market volatility is completely normal, and you will be hit with financial victories and possibly losses throughout your investing career. Continuing to invest throughout the highs and lows of the market is a typical strategy for early career employees.

Mid-Career Employees – 10 to 15 years until retirement

If you are 10 to 15 years from retirement, you still have time to recover from a hard-hitting market. It’s tempting to throw in the towel, stop your contributions or switch to a more conservative investment option when you’re seeing negative returns. However, this may be one of the worst things you do for your account balance. If you sell while the market is in the red or below where you initially bought in, you lock-in your financial losses and could miss the potential gains during the market’s recovery phase. During these unstable times, continue to think long-term. If you have questions or concerns or if you need a simple pep-talk, take 30-minutes to meet with a MO Deferred Comp financial education professional. The team may not have a crystal ball to predict the future, but they do have years of experience and can educate you on your options.

Late Career Employees – Less than 10 years until retirement

It’s okay to worry about your investments when you’re nearing retirement but try to focus on what you can control, like how much you’re contributing to your retirement savings account, and make the most of your working days. This means you may want to consider increasing or maxing-out your contributions during a downturn to take advantage of low market prices. You may also want to slowly tweak your investment strategy to better suit your risk tolerance or even consider converting to Roth while the markets are down. Whatever you decided to do, speak with an education professional to ensure you’re making an informed decision and remember, historically the market has always recovered from a down market. It may just take a few years or longer to fully recoup.

Retired Employees

A down market, plus high inflation, is not exactly a retiree’s dream financial situation. At this point in your life, if you’re like most retirees, you have probably shifted your investment strategy to be fairly conservative and hopefully that is helping protect your savings from some volatility. If you’re in this situation, a few things to consider are how much you’re withdrawing from your account and how you’re spending your income. Prices of goods and services are currently soaring. To avoid over-withdrawing and shortening the lifespan of your savings, having a decumulation strategy and a budget helps control your spending. If you’re particularly concerned about how the stock market is affecting your spend-down strategy and savings, schedule a one-on-one meeting with a deferred comp financial education professional or attend a Retirement Income Spend-down Strategies seminar near you.